Pretty much anyone you talk to has had one experience or another with selling a home and for every one of these experiences there is a different story and different advice on the best way to sell your home. Unfortunately not every one is real  estate expert and there are a lot of myths being spread around about selling a home. We are here to debunk 5 of the most common myths people hear about selling a home.

estate expert and there are a lot of myths being spread around about selling a home. We are here to debunk 5 of the most common myths people hear about selling a home.

Myth 1: If your home sells quickly, you’ve under priced it

If your home sells quickly, it is an indication that you’ve priced it correctly. While setting the price of your home high and gradually lowering it over time can be tempting; generally, it is a bad idea. Setting an unrealistic price will scare off qualified buyers and cause your house to sit on the market longer. There is only a limited amount of time your home’s listing will be considered ‘new’; after that time has expired buyers’ sense of urgency is significantly diminished, and the whole process slows down. A good real estate agent will offer you a comparable market analysis to delineate your home’s true market value and help you to price it appropriately.

Myth 2: Making improvements to your home will increase its sale price

Making improvements to your home can either benefit you or hurt you depending on the circumstances. First of all, don’t go too crazy with the work you do. While making relatively inexpensive improvements such as a new coat of paint on the interior or replanting the flower bed in your front yard are universally recommended and will help you sell your home; more expensive improvements may not actually pay off. For instance, completely refurbishing your kitchen or adding a swimming pool may actually cost you money. Although the improvements may increase the value of the home by $10,000, if they cost $20,000, they’re not worth it. Investment/price discrepancies like this are especially likely to happen if there are not any comparable properties in the area which buyers can use as a baseline to establish a reasonable home value.

Another word of advice with improvements is to keep it simple and neutral. Remember that when selling a home, you’re trying to appeal to the widest cross section of potential buyers possible. So while it’s true that at least a few buyers might like candy apple red walls with bright yellow molding, many more people will be satisfied with beige walls and white molding. Overall, buyers are looking for a home that is move-in ready – in other words – a home that is in good repair, with a clean and neutral look.

Myth 3: Successful sellers don’t negotiate

You shouldn’t view the buyer as your adversary. After all, if you argue with every single potential buyer you meet, you’ll never sell your home. Real estate agents recommend that sellers set their home at a reasonable price and approach the process with a positive attitude. Being willing to make minor compromises can be the difference between selling your home today, and having it sit on the market for another six months.

Myth 4: Buyers are able to clearly see potential in homes that need a little work

Most buyers actually have difficulty seeing the potential in homes that need improvements. This is why many real estate agents recommend that sellers make minor enhancements to their home (such as a fresh coat of paint) before putting it on the market. Most buyers are looking for a home that is ‘move-in-ready’ and making minor repairs/updates can really help speed up the sale of your house.

Myth 5: Advertising is a great way to sell your house

Advertising is used to generate interest in a home, not make it sell. Throwing money at ads for a poorly maintained house will not magically cause it sell. Rather than spend money on advertising, you are far better off researching the correct price for your home and spending your money on any minor repairs/improvements that are necessary. When used in moderation, advertising is a great thing, but you should understand that it will not be the determining factor in the sale of your home; it will only generate interest in it. The home’s condition and price are what the buyer will use to determine whether or not he actually wishes to make the purchase.

That concludes our list of 5 common myths and truths about selling your home and we hope you were able to get some good insight into the home selling process. If you have some myths of your own that we didn’t cover please add them to the comments!

If you are currently in the market for a new home make sure and check out the MoversAtlas.com MoveMap which provides in depth information on real estate, neighborhoods, and their surrounding communities!

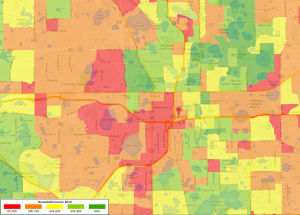

MoveMap, you can see that income figures vary significantly for the Orlando metropolitan area, partly as a function of economics and partly due to simple geographic factors. The Orlando area actually consists of the City of Orlando itself and series of satellite suburban municipalities. These small cities are often called bedroom communities since many of their residents live in them, but work elsewhere; Orlando in this case. This skews the earnings map a bit since people whose incomes are generated by working within the City of Orlando actually live elsewhere. Because median household income is tallied based on where someone lives, many suburban communities have higher median incomes than Orlando itself, where the wages are actually earned.

MoveMap, you can see that income figures vary significantly for the Orlando metropolitan area, partly as a function of economics and partly due to simple geographic factors. The Orlando area actually consists of the City of Orlando itself and series of satellite suburban municipalities. These small cities are often called bedroom communities since many of their residents live in them, but work elsewhere; Orlando in this case. This skews the earnings map a bit since people whose incomes are generated by working within the City of Orlando actually live elsewhere. Because median household income is tallied based on where someone lives, many suburban communities have higher median incomes than Orlando itself, where the wages are actually earned.